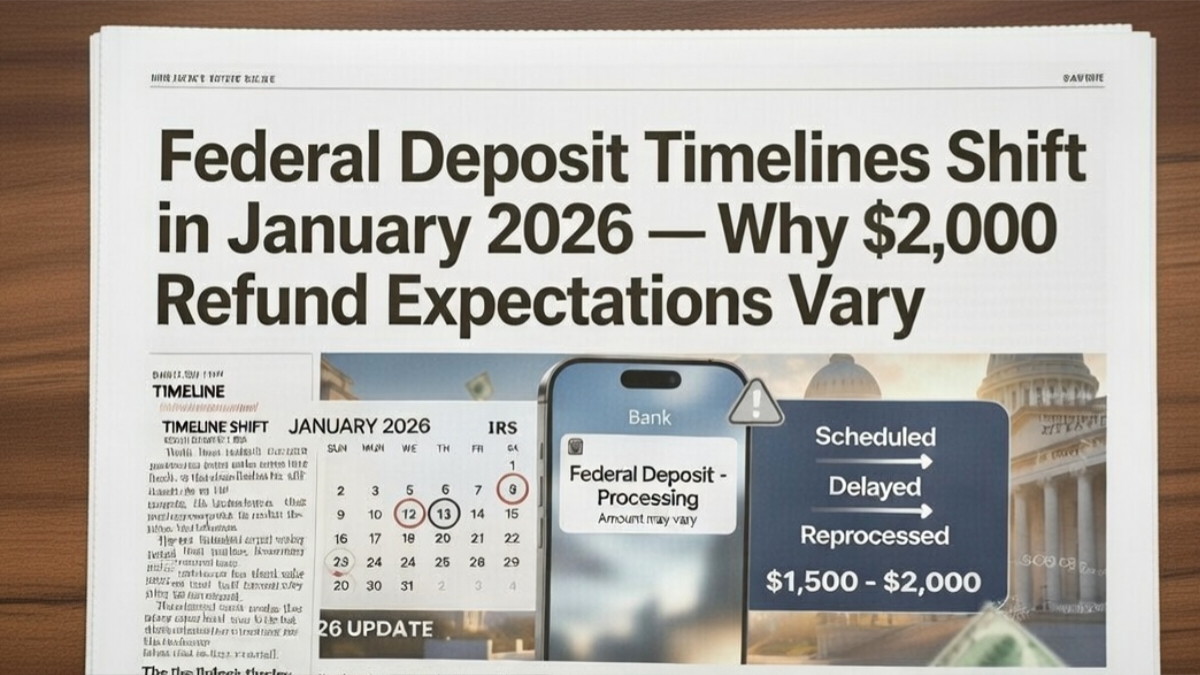

Federal Deposit Timelines Shift in January 2026: As the 2026 tax filing season opened in late January, a familiar sense of anticipation swept across American households. Online forums, short-form videos, and social media posts began circulating claims of an upcoming $2,000 federal payment some framing it as a “refund,” others as a dividend linked to tariff revenue. The confusion has been fueled by a mix of political rhetoric, selective quotes, and a broader public memory of pandemic-era stimulus checks that arrived quickly and with little warning.

In reality, January 2026 marks the start of routine IRS refund processing, not the rollout of a new federal payout. While former President Donald Trump has repeatedly spoken about the idea of sharing tariff revenue with Americans, no law authorising such a payment exists today. This gap between expectation and policy explains why deposit timelines appear inconsistent to many taxpayers. Understanding what is real, what is proposed, and what remains speculative is critical for anyone planning finances in the early months of 2026.

How the IRS Refund System Actually Works in 2026

The Internal Revenue Service officially opened the 2026 filing season on January 26, allowing taxpayers to submit returns for the 2025 tax year. From that point, refund timelines follow long-established administrative processes. For electronically filed returns with accurate information and direct deposit details, refunds typically begin arriving within two to three weeks. Paper returns, by contrast, can take significantly longer, often stretching into early spring.

Refund timing is influenced by more than just filing date. Claims involving refundable credits, identity verification flags, or discrepancies in income reporting often undergo additional review. The IRS has also advised filers to pay close attention to recent tax law changes, including provisions under the One Big Beautiful Bill Act, which could alter refund amounts. Importantly, none of these processes are connected to tariff revenue or special dividend proposals.

The Origins of the $2,000 Tariff Dividend Idea

The notion of a $2,000 tariff-funded payment traces back to remarks made by Donald Trump during 2025 campaign-style appearances and interviews. He argued that aggressive tariff policies could generate enough revenue to both reduce federal debt and return money directly to citizens. The framing deliberately echoed the language of stimulus checks, tapping into a public memory of direct payments received during the COVID-19 crisis.

Despite the attention these statements received, the proposal never moved beyond rhetoric. No formal bill establishing a universal $2,000 tariff dividend has been passed, and no implementing instructions have been issued to the Treasury or IRS. Even allies of Trump have acknowledged that, if such a policy were to materialise, it would likely require months of congressional negotiation and would not realistically appear in early 2026.

Why Refund Expectations Have Become So Distorted

Part of the confusion stems from language. In everyday conversation, “refund,” “rebate,” and “check” are often used interchangeably, even though they refer to distinct mechanisms in federal finance. Tax refunds represent overpaid taxes returned after filing, while stimulus-style payments require new spending authority. When social media posts suggest that “refunds” will include a $2,000 bonus, the distinction is easily lost.

Another factor is historical precedent. Between 2020 and 2021, Congress approved multiple rounds of economic impact payments with extraordinary speed. That experience reset public expectations about how quickly Washington can act. As one fictional policy analyst, Rohan Mehta of the Centre for Fiscal Studies, puts it: “People assume that because it happened once in an emergency, it can happen again casually. That’s not how the budget process normally works.”

Tariff Revenue Reality and Legal Complications

Beyond politics, the numbers themselves present challenges. Independent budget analyses suggest that current tariff collections fall well short of what would be required to fund universal $2,000 payments. Even optimistic projections fluctuate based on trade volumes, global demand, and enforcement outcomes. In simple terms, the revenue stream is neither stable nor large enough to support a guaranteed payout without additional borrowing.

Legal uncertainty adds another layer. Ongoing court challenges to certain emergency tariffs could result in partial refunds to importers, not dividends to households. Treasury Secretary Scott Bessent has acknowledged that such cases, if they reach the Supreme Court, could take a year or more to resolve. These discussions relate to trade law compliance, not to any consumer-facing payment programme.

What Comes Next for Taxpayers and Policymakers

For taxpayers, the immediate takeaway is straightforward. January and February 2026 deposits reflect ordinary IRS refund schedules, shaped by filing choices and return accuracy. Anyone expecting an automatic $2,000 payment tied to tariffs is likely to be disappointed unless Congress acts decisively later in the year. Financial planning should be based on confirmed refunds, not proposed dividends.

On the policy front, the idea of sharing tariff revenue has not disappeared. Bills such as the American Worker Rebate Act of 2025 remain on the table, and election-year dynamics could revive interest in direct payments. However, seasoned observers caution against assuming speed. “Even popular ideas stall without consensus,” notes Mehta. “If something passes, mid-to-late 2026 would be the earliest realistic window.”

Public Sentiment and the Broader Impact

The episode highlights a deeper issue in American fiscal discourse: trust and communication. When high-profile figures float ideas without legislative backing, markets and households alike struggle to separate promise from policy. For lower- and middle-income families, the difference matters. Anticipating money that never arrives can disrupt budgeting decisions, from rent payments to credit card planning.

At the same time, the viral spread of unverified claims underscores the role of digital platforms in shaping economic expectations. Short clips and bold headlines often travel faster than official IRS guidance. Until clearer signals emerge from Congress, the safest assumption remains that 2026 will look fiscally ordinary defined by tax refunds, not surprise dividends.

Disclaimer: This article is intended for informational purposes only and reflects publicly available information as of January 2026. It does not constitute legal, tax, or financial advice. Readers are encouraged to consult official IRS publications or qualified professionals for guidance specific to their individual circumstances.